A. Discharge Rates in Chapter 13

ABI Journal

April 2019

Linda B. Gore

Chapter 13 Trustee

Gadsden, Ala.

Bradford Caraway

Chapter 13 Trustee

Birmingham, Ala.

The success of the implementation of the chapter 13 bankruptcy statute is unquestioned by those who work in this area of law daily and who deal directly with the debtors during their arduous journey through bankruptcy. Chapter 13 trustees routinely receive telephone calls, letters and cards of gratitude from debtors who appreciate the patience, advice and empathy that aided their efforts in bringing their plans to successful conclusions. While a certain percentage of chapter 13 cases might be unsuccessful, when a case is successful, many stakeholders benefit.

Debtors

Debtors who receive a discharge are thankful for the “fresh start” and are justifiably proud of their efforts to pay as much of their debts as possible over the term of the plan. There is nothing easy about successfully completing a chapter 13 plan, and the effort involved requires perseverance and discipline.

One of the primary benefits of filing for chapter 13 is the automatic stay, which allows the debtor some much-needed breathing room for reorganizing their budgets and determining how they shall proceed. The automatic stay also diminishes the constant threats of aggressive collection efforts, which shadow debtors who find themselves in financial straits. An unexamined feature of a successful discharge is the beneficial impact that it might have on the debtor’s psyche: With a discharge, the debtor knows that they have not failed but have worked hard to accomplish the repayment of as much of their debt as they could repay. They did not simply walk away from their obligations, but chose to work through their financial problems with the help of chapter 13. This effort works to restore their self-esteem.

Creditors

Creditors also express gratitude at being able to collect all or a portion of their debts in a process that is overseen by the bankruptcy court and trustee’s office. Overall, the creditors are relieved of the burden and costs of hiring collection agencies or otherwise having to locate debtors. The orderly process of receiving distributions directly from the trustee further saves creditors time and expense.

Domestic-Support Creditors

Domestic-support creditors also routinely call and express thanks for the payments they receive, as they have often given up hope of being paid and feel that the chapter 13 process, with the trustee collecting and disbursing, is the only way they would have been paid on their support claims. Debtors are often tempted to divert these funds elsewhere, but the structure of the chapter 13 plan makes that less likely to happen.

Mortgagors

Mortgagors

One of the most common reasons for a debtor to file a chapter 13 case is to save their home and catch up on the mortgage arrears. When the debtors propose a plan to have the chapter 13 trustee make the ongoing mortgage payments (and curing arrears), the mortgage creditors know that the success rates of chapter 13 cases are much higher than when the chapter 13 debtors make their own mortgage payments. Most mortgage companies are thankful to be receiving mortgage payments this way and are glad to have accurate trustee records of the payments to assist with the reconciliations of their accounts.

Auto Lenders

Another typical reason for a debtor to file for chapter 13 is to save an automobile that might be crucial to the debtor getting and holding a job or necessary to provide family transportation. Section 1325 of the Bankruptcy Code now requires that any automobile purchased within 910 days of the filing of a bankruptcy petition must be paid in full. This provision allows creditors to consider further extensions of credit and ensures that any payment received in bankruptcy will be greater than what they may have received in the past. The impact of this relatively new provision is evidenced by the fact that for the first time in U.S. history, household debt now exceeds $13 trillion.1

In 2017, the latest audited year reported on the U.S. Trustee’s website, chapter 13 trustees disbursed $5,664,096,959 and unsecured claimholders received $1,294,230,468.2 These numbers indicate a healthy, successful program that allows debtors to achieve a “fresh start” while protecting the creditors and helping them receive payments on their debts. Chapter 13 participation meets myriad needs for all parties in the financial community and should be encouraged.

With the passage of the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA), Congress clearly agreed that chapter 13 should be supported, endorsing the mantra that those who could pay their debts should do so. They established the means test to eliminate the chapter 7 choice for debtors with excess disposable income, mandating that those debtors file for chapter 13.

Trustees gather and evaluate tax returns and pay stubs to ensure the accuracy of the case information provided to them. Debtors who belong in chapter 13 are now directed to that chapter so that creditors can be repaid to the greatest extent possible. To support the long-term goals of financial literacy for the debtors as they move forward, mandatory financial programs were set up for debtors exiting bankruptcy to assist them and help avoid a potential return visit to the bankruptcy courts.

Notwithstanding all of the above, chapter 13 has been questioned and criticized of late by academics.3 The criticism stems from the fact that most pundits constantly repeat the trope that “one-third” of all chapter 13 cases do not result in a successful discharge and are dismissed prior to case completion.4 This statistic is offered as an indication of a process that is failing more than succeeding.

Unfortunately, this approach is simplistic and does not paint the full picture of what chapter 13 is, how it works and how success should be measured. This quoted success rate is based on the percentage of debtors who file for bankruptcy who actually get a discharge. A chapter 13 bankruptcy is predicated on the debtor having “regular income,” and debtors sometimes have to file more than one chapter 13 case when a catastrophe or debilitating event (medical emergency, loss of job, divorce, etc.) occurs. These numbers can be misleading when not accounting for that distinction.

Furthermore, the success/failure statistic does not take into account the fact that many debtors voluntarily exit chapter 13 early, since the “time-out” provided by the automatic stay gave them enough time to get back on their feet to where they can repay their creditors 100 percent plus interest without the assistance of bankruptcy. Those debtors are viewed as failures of the system when these figures are quoted, but the debtors might view their time in bankruptcy as successful because it accomplished what they needed it to do.

Hon. Bryan D. Lynch (U.S. Bankruptcy Court (W.D. Wash.); Tacoma), the National Conference of Bankruptcy Judges liaison to the National Association of Chapter 13 Trustees (NACTT), wrote an article suggesting that the success rates should be based on confirmed plans rather than filed cases.5 This crucial distinction is absolutely correct, since chapter 13 trustees have a duty and obligation to request dismissal or conversion of cases that do not belong in chapter 13. Ridding the system of these cases on the front end of the process should be viewed as a success rather than a failure of the trustees or the chapter 13 process.

This oversight is one of the primary responsibilities of a trustee’s office. Chapter 13 trustees routinely move to dismiss cases that exceed the debt limit or are filed by pro se debtors who do not intend to proceed but are merely trying to buy time, plans that do not comply with the Bankruptcy Code, cases and plans that are filed in bad faith for other reasons, or plans that are simply not feasible. Such efforts should be applauded, not discouraged. The statements and views espoused by Judge Lynch are fully adopted here in regard to how the success or failure of chapter 13 should be determined.

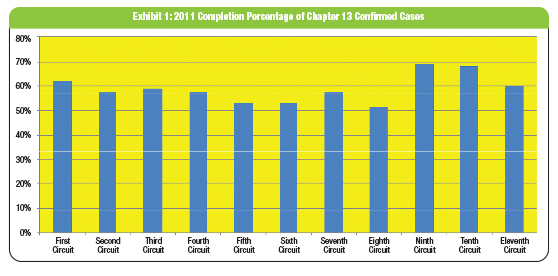

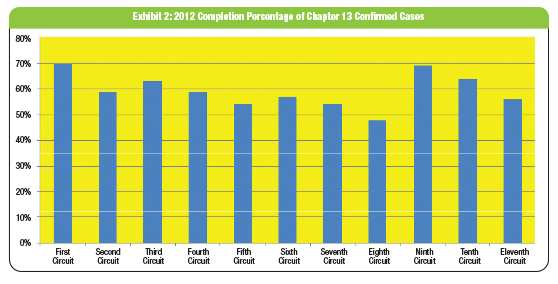

For the last two years, chapter 13 trustees have attempted to determine the success rate of chapter 13 cases based on the discharge rate of confirmed cases instead of filed cases. The authors have polled fellow trustees and asked them to provide the number of cases confirmed and the number of cases discharged for the calendar years 2011 and 2012. These years were chosen because we have to go back to a year where all case outcomes have been decided and no cases are active. We have to go back this far to get complete information, since most chapter 13 cases last at least three years and many last five years.

The result was the same for each year, with a majority of trustees reporting their statistics. Fifty-nine percent of confirmed cases received a discharge, which demonstrates the success of chapter 13. Exhibits 1 (p. 49) and 2 are from each year and show that the percentages changed from circuit to circuit, but the overall percentage stayed the same for each year.

The numbers will continue to be computed yearly so that we can gather the data needed to help ensure that chapter 13 bankruptcies continue to succeed. Chapter 13 trustees in Alabama are studying discharged chapter 13 cases from 2012-13 in an effort to identify common factors that create the best chances for success. This information will be shared with other trustees and the debtor’s bars so that cases with higher chances of success can be identified and that the number of successfully discharged cases will continue to rise.

The NACTT has re-established its statistics committee under the leadership of Kathy A. Dockery, one of the chapter 13 trustees in Los Angeles. The committee’s mission is to keep track of the statistics so we can determine where we are succeeding and where we can improve so that chapter 13 can continue to be the best alternative available for the debtors and creditors.

1 “U.S. Total Household Debt,” Federal Reserve Bank of New York (Nov. 29, 2018), available at ycharts.com/indicators/us_total_debt (unless otherwise specified, all links in this article were last visited on Feb. 25, 2019).

2 “Chapter 13 Trustee Data and Statistics,” U.S. Department of Justice, available at justice.gov/ust/private-trustee-data-statistics/chapter-13-trustee-data-and-statistics.

3 Katherine Porter, “The Pretend Solution: An Empirical Study of Bankruptcy Outcomes,” 90 Tex. L. Rev. 103 (2011).

4 Hon. Brian D. Lynch, “Measuring Success in Chapter 13,” Consider Chapter 13 (June 5, 2016), available at considerchapter13.org/2016/06/05/measuring-success-in-chapter-13.

5 Id.